The quarterly annoucements of monetary policy by the RBI have by now become a huge media event rather like the budget. More often than not, the hype is overdone. But the forthcoming announcement (due on January 31) is of some importance.

Credit has been growing at around 30% in the past three years. Earlier, growth was of the order of 15-16%. The RBI would like to see slower credit growth- the annual statement made at the beginning of FY 2007 had indicated a target growth rate of 20%. There can be two reasons for worrying about high credit growth. One, it could imply a dilution of credit standards and hence hence pose risks of bank failure down the road. Two, by fuelling monetary expansion, it could stoke inflation. How real are these threats in the present situation of the Indian economy?

Bank credit has grown strongly for three reasons. Economic growth has accelerated; there has been a shift in banks' asset portfolios from investments to credit; and banks have woken up to the potential of retail credit.

Retail loans have been growing at 40%. As a result, the share of retail loans in total advances has gone up from 22%in March 2004 to 25.5% in March 2006. Within retail loans, the biggest driver has been home loans. Home loans grew at 50% in 2003-04 and 34% in 2004-05. Home loans account for nearly 50% of all retail loans.

Home loans are loans made to buyers of homes, as distinct from loans to real estate developers. With real estate developers, banks can burn their fingers badly if real estate prices fall (which is quite likely given today's prices). Banks' total exposure to the sensitive sectors (capital market, real estate and commodities) was 19% in 2005-06, with exposure to real estate being the biggest chunk- 17.2%.

Home loans are made against future income, not against assets. If the price that a borrower has paid for a home drops, the borrower does not lose his ability to service the loan: most borrowers are middle-class, salaried individuals. Besides, banks make sure there is reasonable margin to the loans they make: the loan to value ratio can be pegged at 70% or lower. So, even if the value of the home drops, the banks have enough collateral to protect their loans should the borrower default on loan payment. It is these factors that make home loans one of the safest categories of loans for banks. Similar margin protection is available on another important retail loan, loans against shares.

On the wholesale side, banks are not only experiencing lower defaults, they are actualy effecting significant recoveries against loans written off. NPAs have been coming down not only as a proportion of total assets but in absolute terms. Gross NPAs declined from Rs 59,124 crore in March 2005 to Rs 51,815 crore in March 2006. The ratio of net NPA/ total advances of banks of 1.22% is respectable by international standards. In today's buoyant economic conditions, it is hard to see this changing for the worse.

In short, rapid credit growth does not translate into poor loan quality and pose any systemic risk. That is partly because of the particular composition of credit growth: it has a big retail component which is intrinsically high quality.

What about credit growth as a driver of inflation? Money supply has grown at 19%, driven by large credit growth. This is above the growth of 15% targeted by the RBI. But the RBI had projected GDP growth for FY 2007 was for 7.5-8%. We are likely to see growth closer to 8.5%. A case could be made out for money supply expansion to accommodate higher growth.

The RBI, nevertheless, thinks that money supply has still run ahead of the growth rate- it sees clear signs of 'overheating' in the economy. One sign is the inflation rate which has crossed 6%. Another is soaring asset prices. A third sign to watch out for is the current account deficit. How worrying are these signs?

The rise in the inflation rate to over 6% arises partly from the base effect- there was a sharp fall in the wholesale price index around this time last year. The base effect will continue till June. The inflation rate will moderate thereafter as the base effect is corrected and there is, quite possibly, a cut in the oil price in response to the decline in oil prices internationally.

Housing prices may well have peaked. There are signs of a softening of housing prices in some places and the pace of home loans has slackened going by the pronouncements of bank CEOs. Stock prices remain high but these are open to correction at any point.

As for the current account deficit, this is likely to much lower than thought earlier- 1.5% of GDP as against the forecast of 2.5-3% of GDP. So the external front certainly is not showing any effect of 'overheating'in the economy.

This is the backdrop against we the RBI will announce its monetary policy in January 31. A recent development is the ordinance that provides the RBI flexibility to lower the floor for the Statutory Liquidity Ratio to below 25%. Any cut in the SLR makes more funds available to banks for lending. But the RBI is uncomfortable with the present rate of credit growth. So what should the RBI do?

The betting is that any SLR cut will be phase in over a period of time starting from the point when the SLR holdings of banks comes down to 25% from the present level of 29%. This could happen any time in 2007. Thereafter, if the RBI cuts the SLR, banks can have an incremental credit/deposit ratio of 100%.

The RBI might like to slow down credit growth further through a rate hike announcement on January 31. This will help prepare the ground for a cut in the SLR down the road.

For the reasons mentioned above, I do not believe that a generalised rate hike is called for. If particular banks are under-pricing risk or if particular products are being under-priced (such as home loans), then it is best to focus on those segments alone. A generalised rate hike at a time when credit growth may well slow down in response to earlier rate hikes could adversely affect investment down the road.

See my detailed prescription in my ET column.

Thursday, January 25, 2007

Thursday, January 11, 2007

Executive pay: the sky is the limit!

A student at one of the IIMs (not IIMA) is said to have bagged a summer internship for Rs 11 lakh. It is not known whether the internship is in India or abroad (most likely, the latter). What we do know is that Rs 11 lakh would be a top-of-the-line package for domestic placements at the IIMs.

The story made front page news. For the foreign firm, handing out,say,$25,000 for a summer internship means nothing. But the mileage it gets is enormous. So, offering such internships makes sense to foreign firms.

What the soaring offers at IIMs tell us is that executive pay in India is going through the roof. A CEO of a financial services firm told me that he lost an analyst recently to a mutual fund. The analyst, who had less than five years' experience, had a Rs 1 crore offer from a foreign investment bank but turned it down for a lesser pay as fund manager.

The trend-setters in the game are the private equity players. One high-profile investment banker was said to have been lured away last year by a private equity for a packet of $1 million. But that is now passe. A colleague of his has joined another private equity firm on a salary of $2 mn.

We are talking of a salary of Rs 9 crore! Now, Rs 9 crore would profit after tax of a manufacturing firm with sales of Rs 100 crore. For a first generation entrepreneur, it would take some 20 years to get there. An investment banker gets there in the same time but without having take commensurate risks.

This is amazing! What does it mean? It means that the returns to intellectual capital are today as great as those to physical capital. That is exactly what we would expect to see in a knowledge-based economy and in knowledge-intensive sectors. We have already seen the rewards to entrepreneurs in the knowledge-based sectors in the post-reform era- think of Infosys, Biocon and Indiabulls.

You would always expect successful entrepreneurs to reap huge rewards. What is new is that such rewards are now accruing to employees, who are relatively risk-averse- and not just in the knowledge-intensive sectors. A knowledge worker at the senior levels in any firm- anybody who is top management- is making a tidy packet. Today, one paper reports that Cairns India had to pay Rs 100 crore in stock options to persuade an Indian investment banker in London to come to India to head its operations!

News of such payouts draws much outrage. There are, of course, numerous instances of pliable boards making excessively generous payments. But the literature on executive compensation does suggest that there is a competitive market for executive talent. Some of the numbers in the US seem crazy. But, as the search for talent becomes truly global, it should help moderate increases in executive pay. So, I wouldn't get too worked up over the numbers that are bandied about in the media.

See my column on this subject in ET.

The story made front page news. For the foreign firm, handing out,say,$25,000 for a summer internship means nothing. But the mileage it gets is enormous. So, offering such internships makes sense to foreign firms.

What the soaring offers at IIMs tell us is that executive pay in India is going through the roof. A CEO of a financial services firm told me that he lost an analyst recently to a mutual fund. The analyst, who had less than five years' experience, had a Rs 1 crore offer from a foreign investment bank but turned it down for a lesser pay as fund manager.

The trend-setters in the game are the private equity players. One high-profile investment banker was said to have been lured away last year by a private equity for a packet of $1 million. But that is now passe. A colleague of his has joined another private equity firm on a salary of $2 mn.

We are talking of a salary of Rs 9 crore! Now, Rs 9 crore would profit after tax of a manufacturing firm with sales of Rs 100 crore. For a first generation entrepreneur, it would take some 20 years to get there. An investment banker gets there in the same time but without having take commensurate risks.

This is amazing! What does it mean? It means that the returns to intellectual capital are today as great as those to physical capital. That is exactly what we would expect to see in a knowledge-based economy and in knowledge-intensive sectors. We have already seen the rewards to entrepreneurs in the knowledge-based sectors in the post-reform era- think of Infosys, Biocon and Indiabulls.

You would always expect successful entrepreneurs to reap huge rewards. What is new is that such rewards are now accruing to employees, who are relatively risk-averse- and not just in the knowledge-intensive sectors. A knowledge worker at the senior levels in any firm- anybody who is top management- is making a tidy packet. Today, one paper reports that Cairns India had to pay Rs 100 crore in stock options to persuade an Indian investment banker in London to come to India to head its operations!

News of such payouts draws much outrage. There are, of course, numerous instances of pliable boards making excessively generous payments. But the literature on executive compensation does suggest that there is a competitive market for executive talent. Some of the numbers in the US seem crazy. But, as the search for talent becomes truly global, it should help moderate increases in executive pay. So, I wouldn't get too worked up over the numbers that are bandied about in the media.

See my column on this subject in ET.

Indian economy well set now

Does India's recent growth performance represent a cyclical high or does it mark a trend? The debate has been inconclusive thus far but the optimists- to which school I belong- have been gaining ground.

The sceptics say that India is booming only because the world economy is booming; the moment, world economic growth decelerates- and there are any number of reasons this could happen- we will be back to 6% growth. They worry that growth is consumption-driven and this could be spiked by rising interest rates and household debt. They claim there are clear signs of over-heating in the economy. I address these concerns in a recent ET column.

Here, let me dwell a little more on the first argument, namely, that greater integration of the Indian economy with the world economy spells trouble in a global downturn. It is said that the true measure of dependence on the world economy is not just the ratio of exports/GDP. We need to look at (exports+invisible receipts)/GDP because invisible receipts, driven by software exports, have risen fast. The ratio of (exports+invisibles)/GDP has risen from 8.2% in 1990-91 to 24.6%.

True, but experience shows that invisibles are not very elastic with respect to a slowdown in the world economy. Remittances from overseas Indians are not greatly affected by a slowdown. As for software and other invisible exports, these are part of the "off-shoring" phenomenon intended to make overseas firms more competitive. As conditions abroad worsen, one could expect "off-shoring" to rise, not fall, as firms struggle to cut costs.

So the impact of a global slowdown will be adversely felt mainly export of goods. That ratio is now 13%. Let us say that export growth falls by half to 10%. Adjusting for the correspoding fall in imports, India's GDP would decline by 1%, still giving us growth of over 7%. That's why I say that the cyclical component of India's growth should not be overstated.

A key factor underpinning India's improved growth outlook is the increase in the savings rate- from 23.6% in 2001-02 to 29.1% in 2004-05. I believe this figure must have gone up even further. Higher domestic incomes would translate into more saving; there has been further improvement in government finances as measured by the comibined fiscal deficit of the centre and the states; and corporate profits have improved dramatically. I would not be surprised if the next release of figures for savings show a big jump.

Read my ET column on India's growth prospects here.

The sceptics say that India is booming only because the world economy is booming; the moment, world economic growth decelerates- and there are any number of reasons this could happen- we will be back to 6% growth. They worry that growth is consumption-driven and this could be spiked by rising interest rates and household debt. They claim there are clear signs of over-heating in the economy. I address these concerns in a recent ET column.

Here, let me dwell a little more on the first argument, namely, that greater integration of the Indian economy with the world economy spells trouble in a global downturn. It is said that the true measure of dependence on the world economy is not just the ratio of exports/GDP. We need to look at (exports+invisible receipts)/GDP because invisible receipts, driven by software exports, have risen fast. The ratio of (exports+invisibles)/GDP has risen from 8.2% in 1990-91 to 24.6%.

True, but experience shows that invisibles are not very elastic with respect to a slowdown in the world economy. Remittances from overseas Indians are not greatly affected by a slowdown. As for software and other invisible exports, these are part of the "off-shoring" phenomenon intended to make overseas firms more competitive. As conditions abroad worsen, one could expect "off-shoring" to rise, not fall, as firms struggle to cut costs.

So the impact of a global slowdown will be adversely felt mainly export of goods. That ratio is now 13%. Let us say that export growth falls by half to 10%. Adjusting for the correspoding fall in imports, India's GDP would decline by 1%, still giving us growth of over 7%. That's why I say that the cyclical component of India's growth should not be overstated.

A key factor underpinning India's improved growth outlook is the increase in the savings rate- from 23.6% in 2001-02 to 29.1% in 2004-05. I believe this figure must have gone up even further. Higher domestic incomes would translate into more saving; there has been further improvement in government finances as measured by the comibined fiscal deficit of the centre and the states; and corporate profits have improved dramatically. I would not be surprised if the next release of figures for savings show a big jump.

Read my ET column on India's growth prospects here.

Tuesday, January 02, 2007

Upbeat on the world economy

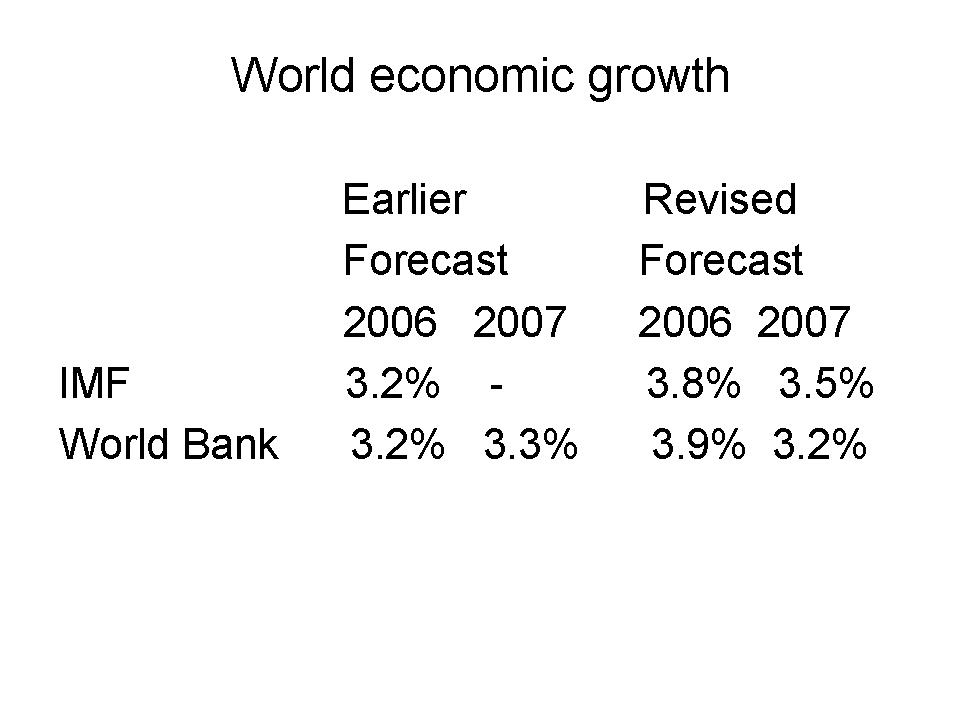

This has turned out to be a better year for the world economy than most people had expected. Both the IMF and the World Bank have revised upwards their projections for 2006. (See table alongside- the IMF forecasts from World Economic Outlook, September 2005 and September 2006; the World Bank forecasts are from Global Economic Prospects 2006 and 2007.). In 2007, both see a deceleration in growth with the IMF projecting a smaller deceleration than the World Bank. Note that the projected growth rates are still above the trend rate of 3% seen in the period 1980-2000.

So, the Cassandras have been proved wrong. They were telling us that the world economy would be on the skids for a number of reasons:

* Oil prices would go cross $100

* America's current account imbalances would unwind in ways that would derail the world economy

* America's housing sector would see a huge bust

So, what happened? Well, American current account imbalances remain. The housing sector has seen a slowdown but not a crash. But the biggest surprise has been oil prices. Oil prices were ruling above $75 in August. They have gone below $60. This is a level that the world economy can shrug off.

The decline in oil prices has meant that inflationary tendencies have been curbed everywhere and interest rate increases in the industrial world, including the US, have not seemed inevitable. In the US, the gradual slowing down of the economy- the much awaited 'soft landing'- has also meant that the US Fed has not been under pressure to raise interest rates.

I believe that one factor, more than anything else, has changed the global economic outlook dramatically: Israel's failed offensive on Lebanon in July.What's the connection?, you might wonder. It goes like this. America had planned an all-out assault on Iran, aimed at decimating Iran's nuclear facilities and defence infrastructure. But before this happened, the Iran-backed militia in Lebanon had to be neutralised. Otherwise, the Hezbollah would react to an American assault on Iran by launching long-distance missiles into the heart of Israel.

The Israelis got the opportunity they were looking for when the Hezbollah abducted two of their soldiers (although this was in retaliation for earlier Israeli abductions). They tried to pulverise the Hezbollah from the air. That didn't work. So they launched a ground offensive. To their chagrin, they ran, not into the sort of ragtag bunch of guerillas they had encountered in the West Bank and Gaza, but a force that was fully prepared for an invasion, well equipped and superbly trained. The offensive was called off.

This meant that war in the Gulf had been averted for the time being. The 'terror premium' built into oil prices vanished and oil prices started climbing down. That gave the world economy a huge boost. It follows that the key risk to the world economy in 2007 is America's policy towards Iran. The Bush-Blair duo faces a humiliating rout in Iraq and might want to salvage its legacy by announcing that Iran has ceased to be a nuclear threat to the world. If that happens, all bets on global economic growth continuing are off.

Barring a US-led war against Iran, the world economy should chug along and there is a good chance that growth will exceed the Fund-Bank forecasts in 2007.

Subscribe to:

Comments (Atom)