The Sensex has recovered somewhat after the fall of nearly 7% last week. It has had a dream run since 1999 producing an annualised return of 23.7%. Will this continue? Many think it will. Swaminathan Aiyar, writing in the Times of India, argues that nominal GDP will grow at around 12.5%. Profits of the better companies will grow at at least 1.5 times nominal GDP. So the Sensex can be expected to grow at 18% in the next years and touch 30,000 whatever the intervening ups and downs.

Is this plausible? I see several problems in Aiyar's formulation. First, sales of top companies may grow faster than GDP but not necessarily profits.

Secondly, earnings growth in recent years are, to some extent, the result of savings in costs, including interest costs. These savings are not entirely sustainable. Besides, there will be earnings dilution arising from funds raised for capital expenditure.

Thirdly, in projecting a Sensex level of 30,000, Aiyar assumes that the current level is right. The P/E for the Sensex is around 24, way above its historical level.

In short, projecting an 18% annual rise in the Sensex from today's level appears unrealistic.

There is also the issue of what sort of returns we can expect from the equity market in the long run. The long-run premium in the US is 5.8%. For the world as a whole, it is 4.9% (based on an index of 16 developed country markets). That is the historical premium. An academic study (which I cite in my recent ET column) projects the future premium at 3%.

If we assume that returns in India over a long period of 20 years (the past seven years plus another 13 years)will approximate returns to a global index, we can most likely expect an annual return of 10% (assuming a 3% risk premium on a risk-free return of 7%). This return, according to the study I cite, has a probability of 50%

There is, of course, a chance that the coming decade will be a unique period of exceptionally high returns in the Indian market. But, going by a study on world-wide stock market returns, the probability that the annual return of 23.7% seen in the past seven years will be sustained is just 10%. There are no miracles in the stock market, you see.

I explore this theme in greater detail in my latest ET column.

Monday, December 18, 2006

Thursday, December 07, 2006

Reforms and growth

There is a fairy tale version of India's economic reforms that has seized the popular imagination. It goes like this. The Indian economy was comatose until 1991. Then, a brave band led by Narasimha Rao (or Manmohan Singh,if you like) strode in and waved a magic wand called 'reforms'. Private entrepreneurs then stepped in where the state had dominated the economy. ZOOM.... the Indian economy took off, never to look back again.

That, as I said, is the popular perception. The academic viewpoint tends to be rather different. It would highlight three key facts:

1. The 'structural break' in India's economic growth, occcured, not in 1991, but in 1980, a full decade before 'reforms' were said to be have been ushered in.

2. Growth accelerated from 6% to 8% in 2003-04 just when people had begun to give up on 'reforms' and were wringing their hands in despair over the opportunities being squandered by the Left-supported UPA government.

3. The state sector and public sector enterprises are very much part of the turnaround story.

Start with the first point. Enough studies have documented the acceleration in growth rate in the eighties to around 6% from the 'Hindu' rate of 3.5% in the preceding decades. In the nineties, the growth rate did not change significantly.

What caused the acceleration in the eighties? Well, there was a definite pro-business orientation and a loosening of controls in the eighties itself- so certain policy initiatives had occurred in the eighties itself, whether you want to call these 'reforms' or not.

What we saw in the nineties was a continuation and extension of policies that had already been initiated in the eighties. While the overall economic growth remained at around 6%, the driver of growth in the nineties was not industry, which had been the primary target of 'reforms', but the services sector. The services sector is much larger than IT- it comprises things such as real estate, finance, tourism, etc, areas that were largely untouched by the nineties' 'reforms'. This is one big puzzle that needs to be cracked by those who believe that it was the nineties' 'reforms' ushered in more rapid growth.

The next big puzzle for the 'reforms' brigade is the performance since 2003-04. The 'reforms' brigade argued that the momentum created by the first round of reforms had been spent and that growth could be accelerated or even sustained only if the 'second generation' reforms were pushed through- labour market reforms, cuts in subsidies, privatisation, downsizing of government, greater FDI, etc.

The UPA government showed itself averse to these. But the rebound in growth in 2003-04, just before the UPA government took over, has been sustained since. How come? The big difference certainly is the increase in savings rate of 5.5 percentage points from 23.5% to 29% of GDP. Of this, nearly 4 percentage points is accounted for by the turnaround in public savings. Increases in savings made higher investment possible and this has caused growth to accelerate. This bears out point (3) above, namely, that the state sector has contributed towards higher growth.

An important aspect of India's growth story is the performance of the IT sector. This contributed to the improvement in the balance of payments in the initial years after reforms. Nobody can deny that the state contributed in a big way to the IT story-through the huge investments in technical education and also through tax breaks.

I believe that lower interest rates are the key element in the India story. There has been a huge surge in foreign inflows- whether through remittances, FII or FDI- and this has caused interest rates to decline. Lower interest rates have caused public savings to rise, they have made exports more competitive and they have fuelled a huge increase in consumption as the demand for retail credit exploded. The surge in foreign inflows, in turn, reflects growing overseas (including NRI) confidence in the Indian economy, confidence created by two decades of sustained growth, not just growth in the nineties.

Taken together, points (1) to (3) make it clear that the Indian growth story is not just about private entrepreneurship having come of age. The story is rather more complex than that and it embraces the state sector as well. So, it is simplistic to suggest that we can now get to 10% simply by rolling back the state even further.

Read my ET column on this subject.

That, as I said, is the popular perception. The academic viewpoint tends to be rather different. It would highlight three key facts:

1. The 'structural break' in India's economic growth, occcured, not in 1991, but in 1980, a full decade before 'reforms' were said to be have been ushered in.

2. Growth accelerated from 6% to 8% in 2003-04 just when people had begun to give up on 'reforms' and were wringing their hands in despair over the opportunities being squandered by the Left-supported UPA government.

3. The state sector and public sector enterprises are very much part of the turnaround story.

Start with the first point. Enough studies have documented the acceleration in growth rate in the eighties to around 6% from the 'Hindu' rate of 3.5% in the preceding decades. In the nineties, the growth rate did not change significantly.

What caused the acceleration in the eighties? Well, there was a definite pro-business orientation and a loosening of controls in the eighties itself- so certain policy initiatives had occurred in the eighties itself, whether you want to call these 'reforms' or not.

What we saw in the nineties was a continuation and extension of policies that had already been initiated in the eighties. While the overall economic growth remained at around 6%, the driver of growth in the nineties was not industry, which had been the primary target of 'reforms', but the services sector. The services sector is much larger than IT- it comprises things such as real estate, finance, tourism, etc, areas that were largely untouched by the nineties' 'reforms'. This is one big puzzle that needs to be cracked by those who believe that it was the nineties' 'reforms' ushered in more rapid growth.

The next big puzzle for the 'reforms' brigade is the performance since 2003-04. The 'reforms' brigade argued that the momentum created by the first round of reforms had been spent and that growth could be accelerated or even sustained only if the 'second generation' reforms were pushed through- labour market reforms, cuts in subsidies, privatisation, downsizing of government, greater FDI, etc.

The UPA government showed itself averse to these. But the rebound in growth in 2003-04, just before the UPA government took over, has been sustained since. How come? The big difference certainly is the increase in savings rate of 5.5 percentage points from 23.5% to 29% of GDP. Of this, nearly 4 percentage points is accounted for by the turnaround in public savings. Increases in savings made higher investment possible and this has caused growth to accelerate. This bears out point (3) above, namely, that the state sector has contributed towards higher growth.

An important aspect of India's growth story is the performance of the IT sector. This contributed to the improvement in the balance of payments in the initial years after reforms. Nobody can deny that the state contributed in a big way to the IT story-through the huge investments in technical education and also through tax breaks.

I believe that lower interest rates are the key element in the India story. There has been a huge surge in foreign inflows- whether through remittances, FII or FDI- and this has caused interest rates to decline. Lower interest rates have caused public savings to rise, they have made exports more competitive and they have fuelled a huge increase in consumption as the demand for retail credit exploded. The surge in foreign inflows, in turn, reflects growing overseas (including NRI) confidence in the Indian economy, confidence created by two decades of sustained growth, not just growth in the nineties.

Taken together, points (1) to (3) make it clear that the Indian growth story is not just about private entrepreneurship having come of age. The story is rather more complex than that and it embraces the state sector as well. So, it is simplistic to suggest that we can now get to 10% simply by rolling back the state even further.

Read my ET column on this subject.

Sunday, December 03, 2006

Microfinance - a trifle hyped up?

The award of the Nobel peace prize for this year to Grameen Bank founder Mohammed Younus has evoked a barrage of peans in praise of microfinance. Here at last, it seems, there is a trusty cure for poverty. Don't give the poor handouts or jobs, let them help themselves by gaining access to credit. Give the poor a loan and you have the makings of an entrepreneur.

I have been rather sceptical of the claims made on behalf of microfinance and found my scepticism reinforced by a recent exchange between two redoubtable economist-bloggers, Richard Posner and Gary Becker, the latter a Nobel laureate himself.

Posner notes that microfinance fills a gap left unfilled by commercial banks who may be averse to taking the risks involved or may be constrained by interest rates they can charge. Microfinance takes over from informal loans made by relatives and clan members. It thus marks a transition from an economy based on trust to one to a normal commercial society.

Having placed microfinance in a conceptual framework, Posner goes to underline its shortcomings:

As a substitute for trust, microfinance has obvious drawbacks. Extremely high interest rates, though justified not only by the risk of default(and the opportunity cost of money, that is, the riskless interest rate) but also by the very high transaction costs of a tiny loan (since those costs are largely fixed,

rather than varying with the size of the loan), burdens the borrower with very heavy fixed costs, since he must repay the loan regardless of the success of his enterprise.....Borrowing at astronomical interest rates seems an unlikely formula for commercial success--and the more unlikely the poorer the borrower......

The evidence for the efficacy of microfinance in stimulating production and alleviating poverty is so far anecdotal rather than systematic. The idea of borrowing one's way out of poverty is passing strange. And I am unaware of any historical examples of nations that climbed out of poverty on the backs of small entrepreneurs financed by credit. Also, recall that Grameen Bank has lent almost $6 billion to some 6 million persons. This implies an average loan of almost $1,000, which in a country like Bangladesh is not chicken feed and makes one wonder how much of the Grameen Bank's loan portfolio is actually microfinance.....

I suggest, albeit tentatively, that there may be a good less to microfinance than its boosters claim.

In his response, Becker says that he does not believe that micro-finance loans are at market rates, that, is they price risk correctly. There is an element of subsidy in microfinance.It is the subsidy element in microfinance that explains why commercial banks have not ventured into micro-loans.

The Grameen Bank and other groups active in making micro loans have had some financing from NGO's that do not seek to make commercial returns on their spending. So my belief is that despite the seemingly "high" interest rates on these loans, they have earned returns, adjusted for servicing, risk, and other costs, that are below market interest rates in their respective countries

On the positive side, Becker notes that a big chunk of microfinance goes to women. To the extent that this enhances empowerment of women, it is welcome. So microfinance should be seen as a more effective way for private groups to make gifts to women that the customary handouts.

Microfinance will begin to make a big impact only when it becomes viable as a for-profit operation. That alone will make it a sustainable business model. It remains to be seen whether this challenge is addressed.

In India, microfinance is still very small in size with an estimated Rs 40 bn of total loans and mostly concentrated in four states in the south. The big impact on poverty will still come through job creation and through financial deepening, that is, commercial banks enlarging their reach and covering the under-served segments of society.

The danger with all the hype about microfinance is that it becomes an excuse for government and bankers to not do their bit- hey, we have microfinance, so why should the government or commercial banks bother about poverty alleviation?

I have been rather sceptical of the claims made on behalf of microfinance and found my scepticism reinforced by a recent exchange between two redoubtable economist-bloggers, Richard Posner and Gary Becker, the latter a Nobel laureate himself.

Posner notes that microfinance fills a gap left unfilled by commercial banks who may be averse to taking the risks involved or may be constrained by interest rates they can charge. Microfinance takes over from informal loans made by relatives and clan members. It thus marks a transition from an economy based on trust to one to a normal commercial society.

Having placed microfinance in a conceptual framework, Posner goes to underline its shortcomings:

As a substitute for trust, microfinance has obvious drawbacks. Extremely high interest rates, though justified not only by the risk of default(and the opportunity cost of money, that is, the riskless interest rate) but also by the very high transaction costs of a tiny loan (since those costs are largely fixed,

rather than varying with the size of the loan), burdens the borrower with very heavy fixed costs, since he must repay the loan regardless of the success of his enterprise.....Borrowing at astronomical interest rates seems an unlikely formula for commercial success--and the more unlikely the poorer the borrower......

The evidence for the efficacy of microfinance in stimulating production and alleviating poverty is so far anecdotal rather than systematic. The idea of borrowing one's way out of poverty is passing strange. And I am unaware of any historical examples of nations that climbed out of poverty on the backs of small entrepreneurs financed by credit. Also, recall that Grameen Bank has lent almost $6 billion to some 6 million persons. This implies an average loan of almost $1,000, which in a country like Bangladesh is not chicken feed and makes one wonder how much of the Grameen Bank's loan portfolio is actually microfinance.....

I suggest, albeit tentatively, that there may be a good less to microfinance than its boosters claim.

In his response, Becker says that he does not believe that micro-finance loans are at market rates, that, is they price risk correctly. There is an element of subsidy in microfinance.It is the subsidy element in microfinance that explains why commercial banks have not ventured into micro-loans.

The Grameen Bank and other groups active in making micro loans have had some financing from NGO's that do not seek to make commercial returns on their spending. So my belief is that despite the seemingly "high" interest rates on these loans, they have earned returns, adjusted for servicing, risk, and other costs, that are below market interest rates in their respective countries

On the positive side, Becker notes that a big chunk of microfinance goes to women. To the extent that this enhances empowerment of women, it is welcome. So microfinance should be seen as a more effective way for private groups to make gifts to women that the customary handouts.

Microfinance will begin to make a big impact only when it becomes viable as a for-profit operation. That alone will make it a sustainable business model. It remains to be seen whether this challenge is addressed.

In India, microfinance is still very small in size with an estimated Rs 40 bn of total loans and mostly concentrated in four states in the south. The big impact on poverty will still come through job creation and through financial deepening, that is, commercial banks enlarging their reach and covering the under-served segments of society.

The danger with all the hype about microfinance is that it becomes an excuse for government and bankers to not do their bit- hey, we have microfinance, so why should the government or commercial banks bother about poverty alleviation?

Friday, December 01, 2006

Much ado about outward FDI

The Tata group's bid for Corus hangs in the balance. When Corus management indicated its acceptance of the Tata offer, the response in India was euphoric. Corporate India, the pundits said, had come of age. Indian companies would now sally forth and conquer. We should soon expect outward FDI to exceed inward FDI.

Calm down, folks. Yes, there will be overseas acquisitions, more so as the rupee appreciates. But not many companies are in a position to bring off deals of this size- they do not have the financial muscle or the stature to put together deals of this order. Others, such as software companies, have chosen to go in for small acquisitions ($50 million or so) because their problem is managing high rates of organic growth.

Not just software companies but those in pharmaceuticals, automotives and bio-tech find they are able to compete in the international marketplace from out of India. Knowing the hassles that go with large acquisitions- the majority of cross-border acquisitions fail to enhance shareholder value- they will play it safe and make relatively small acquisitions.

As for the impact of balance of payments, we need to factor in the following:

i. The bigger deals will be funded overseas, so will not entirely involve outward FDI.

ii. Most acquisitions, as stated above, will be small.

iii. Inward FDI is today very low in relation to the potential of the Indian economy and is bound to rise sharply.

For these reasons, net FDI (inward minus outward) will remain positive.

Read my ET column on the subject.

Calm down, folks. Yes, there will be overseas acquisitions, more so as the rupee appreciates. But not many companies are in a position to bring off deals of this size- they do not have the financial muscle or the stature to put together deals of this order. Others, such as software companies, have chosen to go in for small acquisitions ($50 million or so) because their problem is managing high rates of organic growth.

Not just software companies but those in pharmaceuticals, automotives and bio-tech find they are able to compete in the international marketplace from out of India. Knowing the hassles that go with large acquisitions- the majority of cross-border acquisitions fail to enhance shareholder value- they will play it safe and make relatively small acquisitions.

As for the impact of balance of payments, we need to factor in the following:

i. The bigger deals will be funded overseas, so will not entirely involve outward FDI.

ii. Most acquisitions, as stated above, will be small.

iii. Inward FDI is today very low in relation to the potential of the Indian economy and is bound to rise sharply.

For these reasons, net FDI (inward minus outward) will remain positive.

Read my ET column on the subject.

Thursday, November 30, 2006

Why financial inclusion makes commercial sense

Talk of 'financial inclusion'and many people will start yawning. 'Inclusive growth' is something of a buzzword now and many might be forgiven for supposing that it's one of those expresssions politicians love to include in their speeches. Makes growth look so much more respectable.

Yet, financial inclusion is not something to bracketed with, say, the employment guarantee scheme. I argue in my latest ET column that banks should go for it because it makes excellent commercial sense. Banks have a problem accessing deposits. Reaching out to under-banked areas would help them get low-cost, stable deposits. It would also help them make loans with higher yields than what they can charge corporates today.

Banks have had a cosy time these past few years because of the surge in liquidity and because savers have been wary of the capital market. On the asset side, top borrowers' demand for funds has diminished but banks have substituted them with retail assets. As a result, banks have been able to maintain their net interest margin, the difference between interest income and interest expense as a proportion of assets.

This run of luck won't continue. Banks' net interest margin is bound to come under pressure as savings seek out higher returns in the capital markets and elsewhere and the best borrowers continue to exit the banking system. Financial inclusion could be an excellent bet for banks in commercial terms.

The trick is to get banks to put systems in place to measure risk-adjusted return on capital (Raroc). Thanks to Basel II, banks will know the capital allocated, the denominator in Raroc. They need to get a handle on the numerator as well, the return adjusted for risk. When Raroc is measured and monitored, banks will get their pricing right. And the key to taking risks is largely pricing risk correctly. So, more than re-working priority sector loans, the RBI must push banks towards using Raroc.

Read my ET column.

Yet, financial inclusion is not something to bracketed with, say, the employment guarantee scheme. I argue in my latest ET column that banks should go for it because it makes excellent commercial sense. Banks have a problem accessing deposits. Reaching out to under-banked areas would help them get low-cost, stable deposits. It would also help them make loans with higher yields than what they can charge corporates today.

Banks have had a cosy time these past few years because of the surge in liquidity and because savers have been wary of the capital market. On the asset side, top borrowers' demand for funds has diminished but banks have substituted them with retail assets. As a result, banks have been able to maintain their net interest margin, the difference between interest income and interest expense as a proportion of assets.

This run of luck won't continue. Banks' net interest margin is bound to come under pressure as savings seek out higher returns in the capital markets and elsewhere and the best borrowers continue to exit the banking system. Financial inclusion could be an excellent bet for banks in commercial terms.

The trick is to get banks to put systems in place to measure risk-adjusted return on capital (Raroc). Thanks to Basel II, banks will know the capital allocated, the denominator in Raroc. They need to get a handle on the numerator as well, the return adjusted for risk. When Raroc is measured and monitored, banks will get their pricing right. And the key to taking risks is largely pricing risk correctly. So, more than re-working priority sector loans, the RBI must push banks towards using Raroc.

Read my ET column.

Tuesday, November 07, 2006

India and China: the 1962 war revisited

China's President Hu Jintao is due to make a four-day visit to India starting November 20.There has been some comment on the seeming lack of enthusiasm on the Indian side. Where are Sino-Indian relations headed? I address this question obliquely in my recent column in the Economic Times on the occasion of the 44th anniversary of the Sino-Indian border conflict.

China's growing economic and military power has translated into greater Chinese assertiveness in South Asia. China has followed a policy of 'strategic encirclement' in South Asia: it has forged greater economic and military links with India's neighbours with the objective of ensuring that India is confined to the south Asian space. It has also worked hard for the creation of a south Asian nuclear free zone so that, again, India stays put as a sub-regional power. China justified its relationships with south Asian countries by invoking Panch Sheel. It says it has every right to develop whatever relationship it likes with other sovereign countries.

Fair enough. But how does China justify its clandestine support to Pakistan's nuclear weapons programme all these years? More help on the nuclear front is on the agenda when Hu visits Pakistan before he arrives here.

It is the China factor, more than any other consideration, that explains India's gradual drift towards a closer relationship with the US, a process started by the NDA government and carried forward by the UPA government. That is what explains Manmohan Singh's single-minded pursuit of the Indo-US nuclear in the face of considerable scepticism within the country and at the risk of alientating some of India's friends in the non-aligned and Muslim world.

China's attempts at 'strategic encirclement' will now be countered by India becoming a partner in American attempts at containing China, an exercise in which Japan, the east Asian countreis and some of the central Asian republics will be the other partners.

Read my full article in ET here.

Incidentally, I had promised people that this blog would not be just about banking and the Indian economy. I have been true to my word!

China's growing economic and military power has translated into greater Chinese assertiveness in South Asia. China has followed a policy of 'strategic encirclement' in South Asia: it has forged greater economic and military links with India's neighbours with the objective of ensuring that India is confined to the south Asian space. It has also worked hard for the creation of a south Asian nuclear free zone so that, again, India stays put as a sub-regional power. China justified its relationships with south Asian countries by invoking Panch Sheel. It says it has every right to develop whatever relationship it likes with other sovereign countries.

Fair enough. But how does China justify its clandestine support to Pakistan's nuclear weapons programme all these years? More help on the nuclear front is on the agenda when Hu visits Pakistan before he arrives here.

It is the China factor, more than any other consideration, that explains India's gradual drift towards a closer relationship with the US, a process started by the NDA government and carried forward by the UPA government. That is what explains Manmohan Singh's single-minded pursuit of the Indo-US nuclear in the face of considerable scepticism within the country and at the risk of alientating some of India's friends in the non-aligned and Muslim world.

China's attempts at 'strategic encirclement' will now be countered by India becoming a partner in American attempts at containing China, an exercise in which Japan, the east Asian countreis and some of the central Asian republics will be the other partners.

Read my full article in ET here.

Incidentally, I had promised people that this blog would not be just about banking and the Indian economy. I have been true to my word!

Friday, October 13, 2006

Twinkle, twinkle, banking star

| ||||||||||||||||||||

Bank stocks are back in favour. Consider the relative performance of the Bankex, the index for the banking sector in India, and the Sensex, the market index. In the six months upto September 2006, the Bankex underperformed the Sensex. In the last one month, the Bankex has outperformed the Sensex. Why so?

I can think of three reasons:

- There are signs of a softening of interest rates over the past month with oil prices trending downwards.

- In April, the RBI, in its annual credit policy statement, declared its intention to slow down credit growth from 30% in the previous year to 20% in 2006-07. So far, that hasn't happened- credit growth year on year upto stayed at over 30%.

- The last quarter GDP growth turned out to be higher than expected-8.9%. This has caused many forecasters to believe that GDP is more likely now to end up at the upper end of the 7.5-8% band they had projected. Bank stocks are a play on the economy, so what's good for the economy is good for bank stocks.

A buoyant economy boosts volume growth, of course, but it helps in other ways as well. Non-performing assets (NPAs) at banks tend to decline- and we must remember that asset quality in Indian banking is at its best today. There is no imminent danger of this being reversed because leverage among Indian firms is at its lowest in years- 1.06 according to Brics Securities. (Indeed, over the past couple of years banks have been effecting impressive recoveries from past NPAs.) The rising proportion of housing loans in the overall portfolio also makes for improved asset quality.

Secondly, when economic activity is high, so are float funds in the system. These tend to lower banks' cost of funds. That explains why banks' net interest margins (the difference between interest income and interest expense as a proportion of assets) have remained steady or even gone up in some instances despite an increase in interest rates. Higher interest rates on term deposits are offset by the lower cost on CASA (current and savings accounts), the proportion of which tends to go up with increased economic activity.

I have said elsewhere that Indian banking enjoys what would be regarded as an 'impossible trinity' in banking- high volume growth, high asset quality and high net interest margins. What I have stated above sheds light on why this is so. Bank investors, rejoice!

Wednesday, October 11, 2006

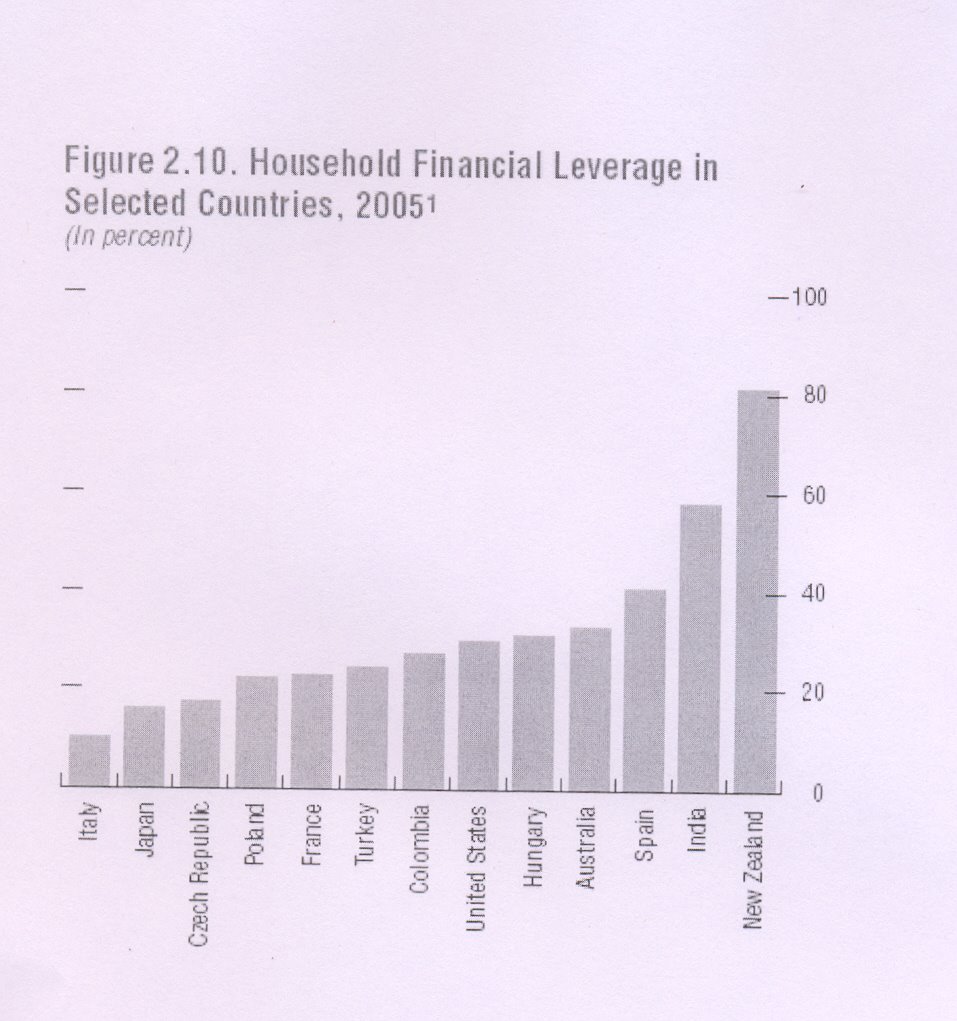

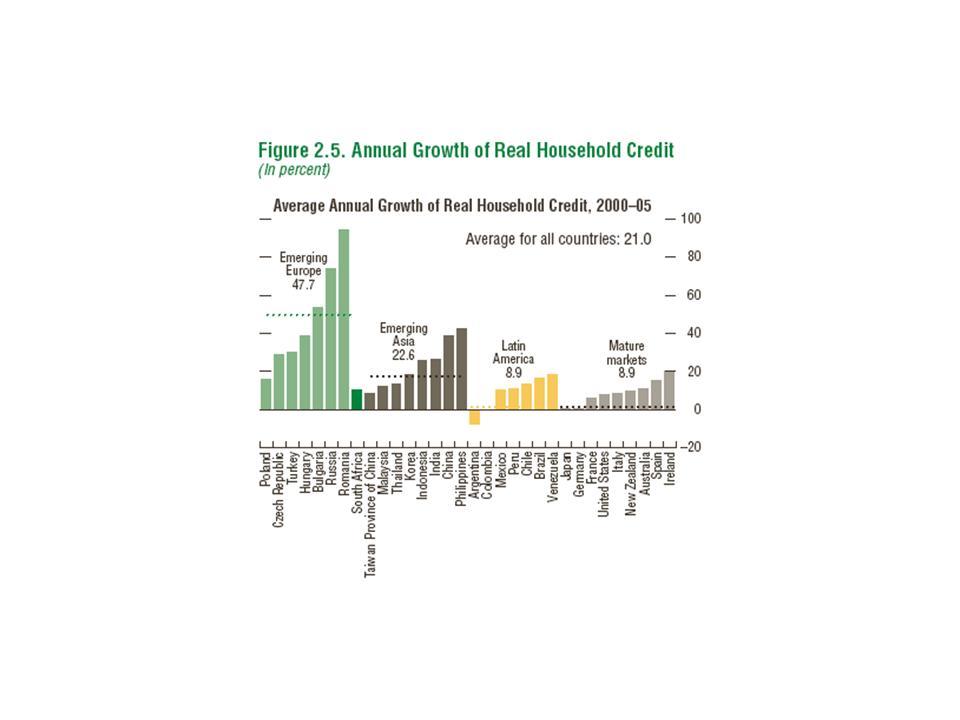

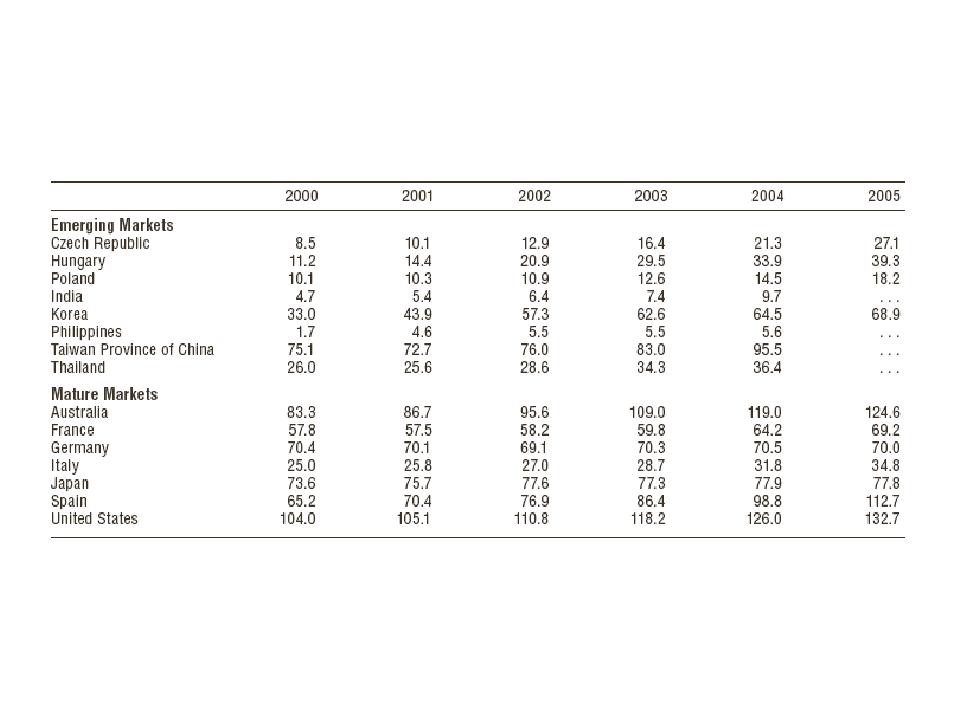

Household credit: how India stacks up

Retail or household credit in India has been growing at breakneck speed. In 2000-05, 25% of the incremental credit came from retail credit. For some banks, retail credit has been as high as 50-70% of additional loans. Is this sustainable? Does it spell trouble for banks, meaning, high non-performing assets down the road?

Answer to the first question: we should expect to see a slowing down because growth is now taking place on a higher base. Secondly, demand for credit from corporates has revived strongly, so banks can expect to grow their portfolios with a better balance between wholesale and retail credit.

As for the second question, the IMF's Global Financial Stability Report (September, 2006) has figures and tables that help place household credit in India in perspective.

The salient points in the two figures and one table reproduced above:

- While retail credit has grown strongly in India, growth is still lower than in emerging Asia and emerging Europe.

- Household credit as a proportion of disposable income in India is the second lowest (after Korea) among a sample of emerging as well as mature markets.

- Household leverage in India is the second highest among a sample of countries, after New Zealand.

Should we worry about high leverage in Indian households? Not really. For at least three reasons:

- The overall figure for leverage is an average across highly indebted rural households and urban ones. It does not give a correct picture of the segments banks are targeting for retail credit- salaried professionals and high net worth individuals

- Most loans are made against future income, not assets

- The biggest chunk of retail loans (nearly 50% of retail exposure) is housing loans on which defaults are- and banks have a solid collateral.

The bottomline: household credit in India can continue to grow strongly without posing problems for the banking sector.

Sunday, October 08, 2006

Credit growth in India: don't push the panic buttons yet

Rapid credit growth gives regulators an attack of nerves- they tend reflexively to associate these with a coming bust. To regulators, runaway credit growth is a sure sign that bankers are compromising on credit quality and that massive non-performing assets will follow.

Scheduled commercial banks' commercial credit- or 'non-food credit' as it is called- grew at 30.8% year on year in 2005-06. This was on top of growth of 28.8% in same period in 2004-05. There is little sign of a slowdown in 2006-07- in July 2006, y-o-y growth was 32.9%.This appears to have the RBI a trifle worried. It would like to see credit growth slowing down to 20% in the coming year.

I believe this concern is a trifle overdone. It's not aggregate credit growth alone that matters. You need to look at three factors: the composition of credit (especially corporate versus retail, exposure to sensitive sectors); the sources of funds for banks (domestic currency versus foreign currency); and whether there are signs of macroeconomic balances. I argue in my column in the

Economic Times that, viewed in relation to these factors, the credit growth we are seeing does not warrant undue concern.

I didn't have a chance to mention in my column that the RBI itself took a rather benign view of credit expansion in its Report on Trend and Progress in Banking in India (2004-05)- box on page 68. It noted that credit expansion in 2004-05 was more broad-based than in the previous years, with credit to industry and agriculture joining the retail sector in driving the demand for commercial credit. It also noted that NPAs in the retail sector, which has provided some of the impetus to credit growth, are still low- around 2%. "Therefore", the RBI concluded, " if banks put adequate risk monitoring and management systems in place, there should not be much cause for concern for the future, although past performance may not always be a good guide".

This was in the Report released in November 2005. Maybe the RBI reckons that three years in a row of rapid credit growth is a bit too much. Remember, however, that GDP growth continues to be robust.Let me qualify my upbeat assessment by saying that, while credit growth may not pose systemic risks, some banks could be asking for trouble.

At least some of the lending rates point to under-pricing of risk by public sector banks. They have responded to rate cuts effected by some of the savvier private banks. But the private banks know what they are doing. They have systems to measure return on capital for any given borrower, retail or wholesale. Not so the public sector banks. The RBI's response has been to increase risk weights for various retail loans. That should cause errant banks to take a closer look at their pricing. But there could be banks out there that fail to make the link between capital allocation and pricing.

Scheduled commercial banks' commercial credit- or 'non-food credit' as it is called- grew at 30.8% year on year in 2005-06. This was on top of growth of 28.8% in same period in 2004-05. There is little sign of a slowdown in 2006-07- in July 2006, y-o-y growth was 32.9%.This appears to have the RBI a trifle worried. It would like to see credit growth slowing down to 20% in the coming year.

I believe this concern is a trifle overdone. It's not aggregate credit growth alone that matters. You need to look at three factors: the composition of credit (especially corporate versus retail, exposure to sensitive sectors); the sources of funds for banks (domestic currency versus foreign currency); and whether there are signs of macroeconomic balances. I argue in my column in the

Economic Times that, viewed in relation to these factors, the credit growth we are seeing does not warrant undue concern.

I didn't have a chance to mention in my column that the RBI itself took a rather benign view of credit expansion in its Report on Trend and Progress in Banking in India (2004-05)- box on page 68. It noted that credit expansion in 2004-05 was more broad-based than in the previous years, with credit to industry and agriculture joining the retail sector in driving the demand for commercial credit. It also noted that NPAs in the retail sector, which has provided some of the impetus to credit growth, are still low- around 2%. "Therefore", the RBI concluded, " if banks put adequate risk monitoring and management systems in place, there should not be much cause for concern for the future, although past performance may not always be a good guide".

This was in the Report released in November 2005. Maybe the RBI reckons that three years in a row of rapid credit growth is a bit too much. Remember, however, that GDP growth continues to be robust.Let me qualify my upbeat assessment by saying that, while credit growth may not pose systemic risks, some banks could be asking for trouble.

At least some of the lending rates point to under-pricing of risk by public sector banks. They have responded to rate cuts effected by some of the savvier private banks. But the private banks know what they are doing. They have systems to measure return on capital for any given borrower, retail or wholesale. Not so the public sector banks. The RBI's response has been to increase risk weights for various retail loans. That should cause errant banks to take a closer look at their pricing. But there could be banks out there that fail to make the link between capital allocation and pricing.

IDBI-UWB Merger

The merger of IDBI with United Western Bank (UWB)is through. IDBI intends to treat UWB as a separate business unit. That makes sense. The arm's length relationship will enable IDBI to cash in on UWB's strengths- high quality customer service, rural loans- without IDBI's having to

tackle the people issues that a merger will entail. Once some of the stressed assets are recovered and UWB is put on a sound footing, the full value of the merger will become evident- and IDBI's price should appreciate.

My initial comments on the merger in my ET column.

tackle the people issues that a merger will entail. Once some of the stressed assets are recovered and UWB is put on a sound footing, the full value of the merger will become evident- and IDBI's price should appreciate.

My initial comments on the merger in my ET column.

Friday, September 08, 2006

Going slow on convertibility

The RBI made public the Tarapore committee report on Capital Account Convertibility (CAC) late August. Even "fuller" convertibility than we have now isn't going to happen soon, if the authorities accept the recommendations of the committee. It will happen in three phases starting: Phase I-2006-07. Phase II: 2007-09 and Phase II- 2009-11. Considering the downside risks to CAC, that is just as well.

I have commented on the report in my column in the Economic Times.

There are some points I didn't have a chance to make in my column:

I have commented on the report in my column in the Economic Times.

There are some points I didn't have a chance to make in my column:

- PNs: The Finance ministry is reluctant to phase out PNs because of the likely impact on the stock market. This is being myopic. It is far more important to ensure the integrity of the financial system and to show that you are practicing “zero tolerance” in respect of KYC norms. Over the long run, this will do a lot to inspire confidence in the Indian financial system and encourage inflows. The benefits will outweigh whatever we gain from the surge in PNs at the moment. The RBI has taken a tough line towards banks found to flouting KYC norms in the IPO scam. It would be inappropriate to practise laxity in this respect towards foreign investors at the same time.

I said in my piece that the answer to the PN issue may to allow direct investment by non-residents right away. But this presumes that we are confident about banks’ grip on KYC. If we are uncertain about this, it is better to defer direct investment by non-residents. - Banking system: Tarapore II wants industrial houses to be allowed to set up banks- with immediate effect, something that surprises even ultra-liberaliser and dissenting member Surjit Bhalla. This would be a major departure for RBI. I can’t see how this can be done without violating the ceiling of 10% on ownership in private banks and the requirement of diversified ownership.

- Data: The committee has asked for liberalisation of outward remittances by Indians going up to $200,000 in the last phase. What has been the experience with the current limit of $25,000? Do we have data? Perhaps we should have a norm for such outflows in relation to reserves/imports. And, of course, we should have the capacity to monitor and cut-off outflows- a real-time monitoring system that can be acted up on in times of crises.

Subscribe to:

Posts (Atom)