Retail or household credit in India has been growing at breakneck speed. In 2000-05, 25% of the incremental credit came from retail credit. For some banks, retail credit has been as high as 50-70% of additional loans. Is this sustainable? Does it spell trouble for banks, meaning, high non-performing assets down the road?

Answer to the first question: we should expect to see a slowing down because growth is now taking place on a higher base. Secondly, demand for credit from corporates has revived strongly, so banks can expect to grow their portfolios with a better balance between wholesale and retail credit.

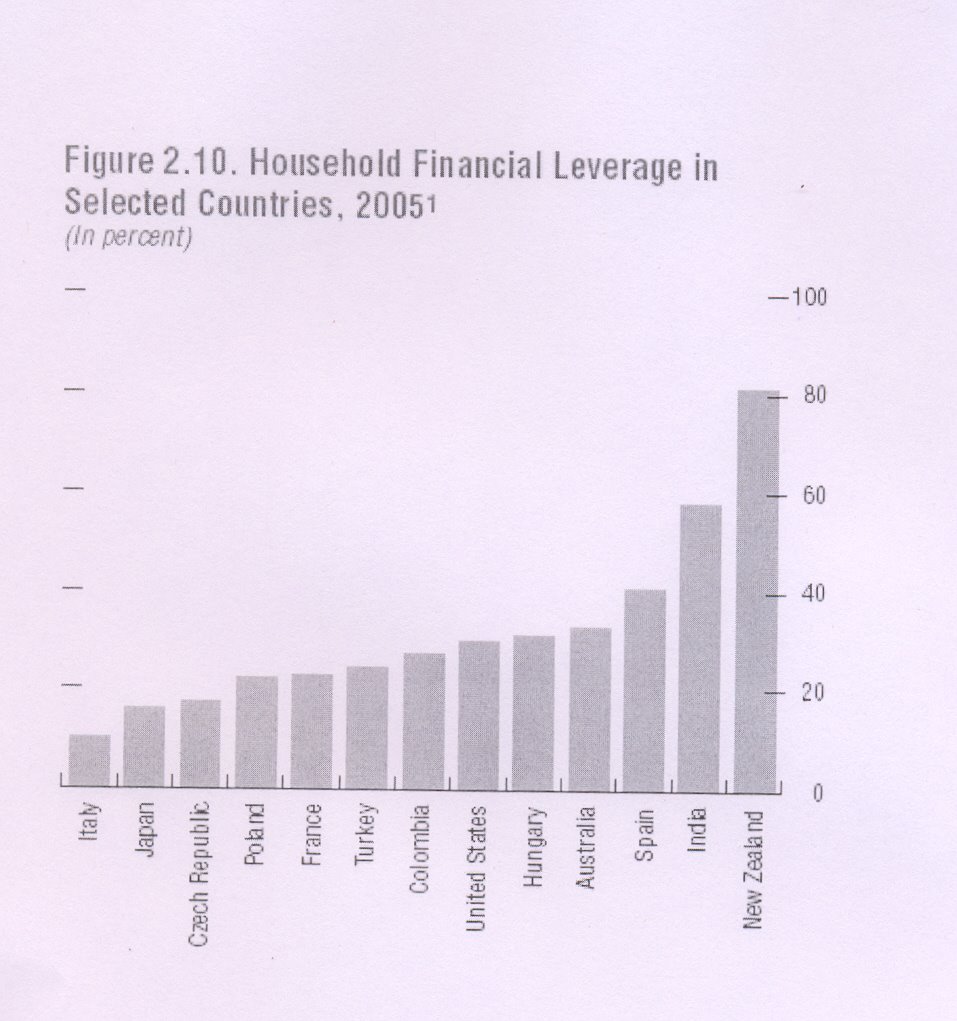

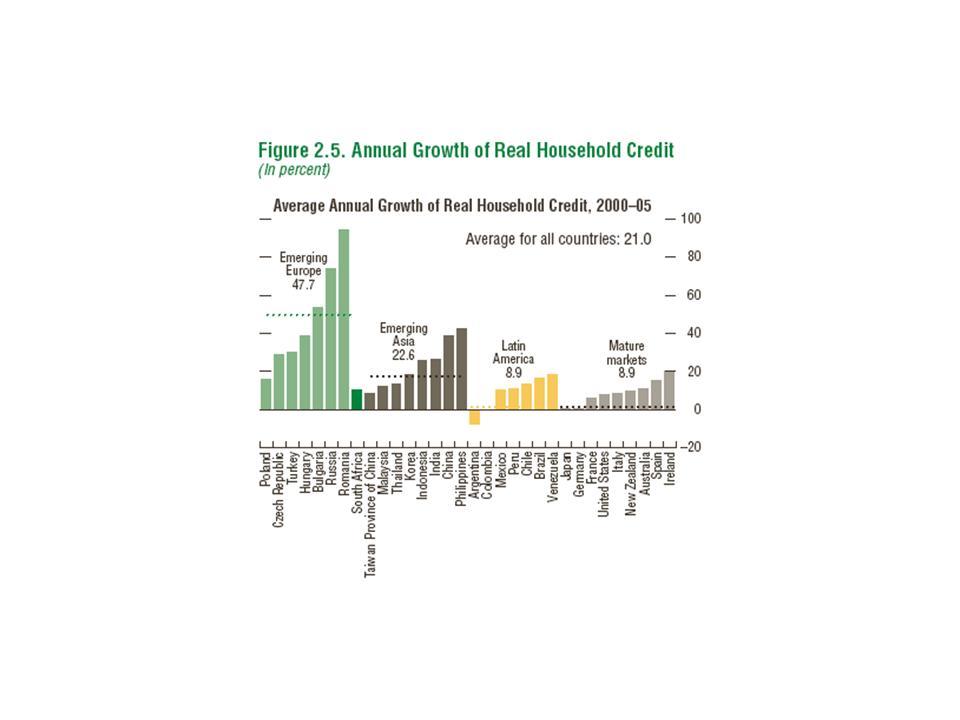

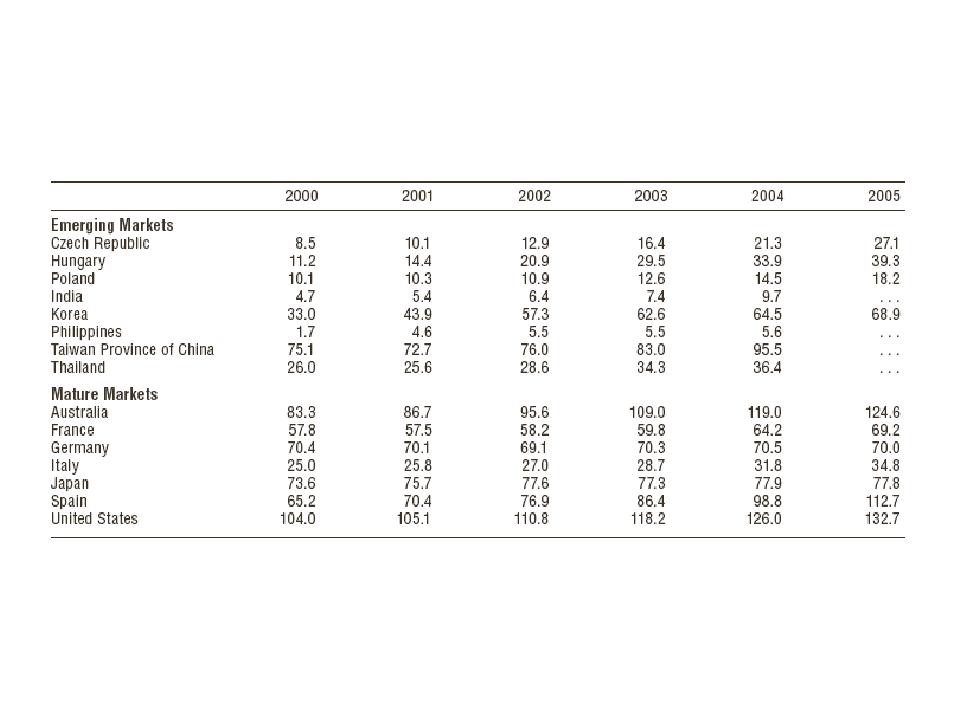

As for the second question, the IMF's Global Financial Stability Report (September, 2006) has figures and tables that help place household credit in India in perspective.

The salient points in the two figures and one table reproduced above:

- While retail credit has grown strongly in India, growth is still lower than in emerging Asia and emerging Europe.

- Household credit as a proportion of disposable income in India is the second lowest (after Korea) among a sample of emerging as well as mature markets.

- Household leverage in India is the second highest among a sample of countries, after New Zealand.

Should we worry about high leverage in Indian households? Not really. For at least three reasons:

- The overall figure for leverage is an average across highly indebted rural households and urban ones. It does not give a correct picture of the segments banks are targeting for retail credit- salaried professionals and high net worth individuals

- Most loans are made against future income, not assets

- The biggest chunk of retail loans (nearly 50% of retail exposure) is housing loans on which defaults are- and banks have a solid collateral.

The bottomline: household credit in India can continue to grow strongly without posing problems for the banking sector.

2 comments:

Dear Prof. T.T.Ram Mohan,

My compliments on an excellent blog. I hope to read many more contrarian views here.

It is heartening that retail credit is only 9.7% of disposable income in India, as compared to 126% in the U.S.A., where the middle classes seem to have embraced Charvaka's instruction "Rinam kritwa ghritam pibet" wholeheartedly. Do we want to become an economy driven by debt and spending?

And where do Indians farmers figure in this figure? I suppose they spend many hundred percent of their disposable income?

I am an entomologist, so I apologise for my laymanlike comments on economic matters. But ant colonies, too, have a sort of economic system, though based on thrift, not debt.

Regards,

Tumbaru

Thanks, Tumbaru, for your kind sentiments. It's a pleasant surprise to know that banking matters are of interest to an entomologist!

About farmers, yes, as I mention in my write-up, they are probably up to the neck in debt. As for the middle-classes, I would reckon they still err on the cautious side. Remember, 50% of retail loans is housing loans. So they are borrowing in a good cause!

-TTR

Post a Comment